Your Most Expensive Mistakes Might Be Correctable

Smart Investors Still Underperform, What to Do About It

The Behavior Gap

Over the course of my career, I have sat across from some extraordinarily accomplished people. Surgeons. Executives. Business owners who built something from nothing. People who have outperformed in every arena that demanded their attention.

And yet, when it comes to investing, many of them share a quiet, nagging suspicion that they are somehow leaving money on the table. They are right. But the reason usually surprises them.

It is not that they chose the wrong funds or the wrong stocks. It is not that they missed a particular sector. It is not even that they paid too much in fees, though that matters. The single most expensive mistake most wealthy investors make is behavioral. It is the gap between what the market returns and what they actually keep.

Researchers call it the Behavior Gap. I can tell you it is real, it is persistent, and it is almost entirely avoidable.

A Small Number That Compounds Into a Large Problem

The S&P 500 has delivered roughly 10% annually over long stretches of history. DALBAR, a firm that has tracked investor behavior for more than three decades, consistently finds that the average equity fund investor earns meaningfully less, closer to 6% to 8% annually, depending on the measurement period.

Two percent. Maybe three. It does not sound catastrophic. Until you let it compound.

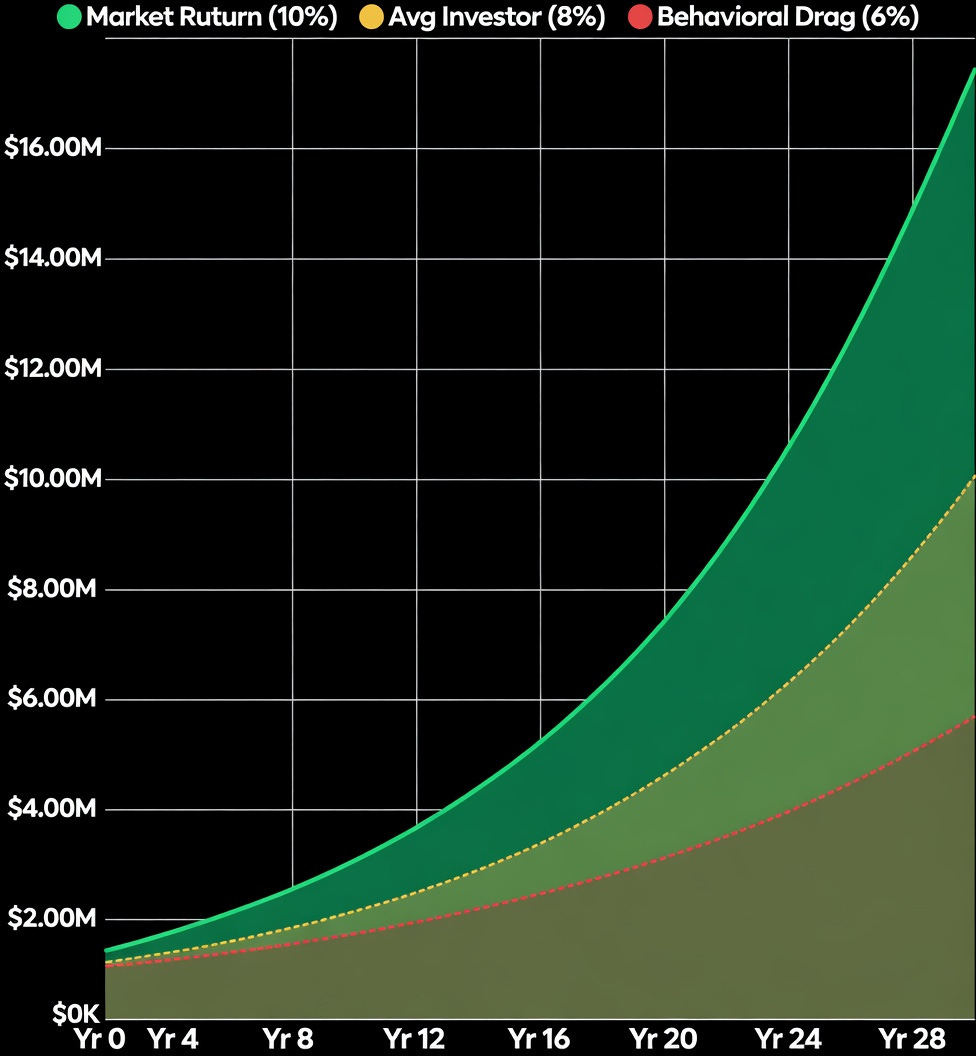

The Compounding Cost of Underperformance

A 2% annual gap doesn’t cost you 20% of your outcome, it can cost you nearly half. Starting with $1,000,000 at 10% annual return grows to ~$17.4M over 30 years. At 8%, roughly $10M. At 6%, approximately $5.7M. The gap is not theoretical, it is the retirement you planned for versus the one you’ll have.

Data source: Historical S&P 500 total returns: Federal Reserve FRED (fred.stlouisfed.org) or Morningstar. Investor return figures: DALBAR Quantitative Analysis of Investor Behavior, annual edition (dalbar.com).

The math is humbling. A two-percentage-point drag sustained over 30 years does not cost you 20% of your outcome. It costs you nearly half. The market was generous. The behavior was not.

This Is Not an Intelligence Problem

Here is what makes the Behavior Gap genuinely frustrating: it does not discriminate by sophistication.

A March 2025 study published in the Journal of Financial Planning surveyed 1,000 investors, comparing those with over $1 million in investable assets to those with between $250,000 and $999,999. The results were striking: high-net-worth individuals indicated higher levels of subjective financial knowledge, but were no less likely to have made investment mistakes due to emotions, suggesting the high-net-worth cohort displayed overconfidence in their abilities.

“More knowledge. Same emotional mistakes.”

The wealthy investors in that study were more confident in their abilities. They spent more time managing their portfolios. And yet, when emotions entered the picture, a volatile market, a geopolitical shock, a bad quarter; they made the same reactive decisions that hurt less sophisticated investors. The playing field was level in the worst possible way.

This pattern has a name in behavioral finance: overconfidence bias. High achievers are particularly susceptible to it because their professional success is real. The skills that built their wealth are not the same skills that protect and compound it.

Four Common Behaviors Cause the Gap

The Behavior Gap is not created by a single catastrophic decision. It is the accumulation of smaller, recurring errors; each one reasonable in the moment, each one costly in aggregate.

1. Performance Chasing

When an asset class has had a strong three-year run, it attracts capital. That is human nature. We extrapolate the recent past into the future. The problem is that by the time an investment appears on your radar as a “winner,” the return has often already been made. The money that floods in near the top is the money that suffers during the correction.

The Timing Problem: Fund Flows vs. Market Returns

Investors consistently pour money in near peaks and pull it out near troughs, buying high and selling low by following emotion rather than discipline. Facts.

Data source: Net equity mutual fund flow data: Investment Company Institute, monthly reports (ici.org). Annual S&P 500 total returns: Standard & Poor’s, Morningstar, or Federal Reserve FRED.

2. Panic Selling

Markets drop. Sometimes sharply. And in those moments, the brain, wired for survival, not wealth accumulation, treats a portfolio decline the same way it treats physical danger: get out. Investors who sold in March 2020 when the S&P 500 fell 34% in five weeks felt rational. They were preserving capital. Many missed the subsequent 12-month recovery of over 70%. The cost was not just the loss. It was the recovery they never participated in.

3. Over-Adjustment

The inverse of panic selling is compulsive tinkering. Some investors respond to uncertainty by continuously repositioning — shifting allocations, swapping managers, moving in and out of cash. Each individual decision may seem sound. Cumulatively, they generate transaction costs, tax drag, and the near-certain outcome of buying and selling at inopportune moments. Do you personally know any wealthy, amateur day traders?

4. Lack of Process

Perhaps the most underappreciated driver of the Behavior Gap is the absence of a systematic framework that removes emotion from the decision-making loop entirely. Research from Vanguard has estimated that behavioral coaching alone can add roughly 150 basis points in net annual return. DALBAR has consistently found that investors underperform markets by an average of 300 basis points annually, largely due to selling low and buying high.

The Rebalancing Blind Spot

One finding from a 2025 study in the Journal of Financial Planning deserves special attention, because it surprised even the researchers: there were no discernible differences in rebalancing behaviors between high-net-worth and affluent respondents. Only 45% of high-net-worth individuals proactively rebalanced their portfolios annually. This was unexpected, given that wealthier investors were more likely to have a formal financial plan and work with a professional advisor.

Rebalancing is not glamorous. But the discipline of selling what has become expensive and buying what has become cheap, enforced mechanically and on a schedule, is one of the few free lunches in investing. Vanguard’s research suggests systematic annual rebalancing can add up to 14 basis points in incremental annual return. More importantly, it enforces the one behavior that separates disciplined investors from reactive ones: buying low and selling high, by design rather than luck.

Portfolio Drift: What Happens When You Don’t Rebalance

Without rebalancing, a 60/40 portfolio silently becomes 75/25 or 80/20 over a strong equity bull market, exposing the investor to risk they never consciously agreed to take. You’re not (necessarily) a great investor, you’ve simply proved the risk/reward thesis.

Data source: Annual S&P 500 total returns (equity) and Bloomberg U.S. Aggregate Bond Index returns (bonds): Federal Reserve FRED (fred.stlouisfed.org), Morningstar, or Bloomberg. Model the drift manually in Excel. Reference: Kinniry et al., “Putting a Value on Your Value: Quantifying Vanguard Advisor’s Alpha” (2022).

What Wealthy Investors Get Right — and What Gets in the Way

The same 2025 FPA study1 found something encouraging: among respondents who use a sounding board or get a second opinion, wealthier individuals were more likely to report their advisor “keeps my emotions in check.” That language matters. It is not just about asset allocation or tax efficiency, it is about the human value of a process that insulates decisions from the emotions that erode them.

Approximately 84% of the high-net-worth cohort was very or somewhat interested in improving their financial skills, which suggests that the appetite for better outcomes is genuine. The gap is not in intention. It is in execution.

The investors I have seen build and preserve generational wealth are not necessarily the ones who were the smartest in the room. They are the ones who built a process, delegated the decisions most vulnerable to emotion, and stayed disciplined during the moments when every instinct told them to act.

Clarity is not something you generate in a moment of market stress. It is something you earn in advance, through planning, through structure, through the humility to recognize that even the most accomplished people need a counterweight to their own instincts.

Ready to Close Your Behavior Gap?

The Behavior Gap is not a market problem. It is a process problem. And the good news about process problems is that they have solutions.

If you have ever looked at your long-term returns and felt a quiet disconnect between what the market produced and what you actually experienced, start bridging the gap

The market will always be unpredictable. Your response to it doesn’t have to be.

Sources & Data References

Sommer, M. & Lutter, S. (2025). “An Exploratory Study of the Wealthy’s Investment Beliefs, Preferences, and Behaviors.” Journal of Financial Planning, 38(3), 56–71.

DALBAR Quantitative Analysis of Investor Behavior, annual edition. dalbar.com

Kinniry, F.M. et al. (2022). “Putting a Value on Your Value: Quantifying Vanguard Advisor’s Alpha.” Vanguard. advisors.vanguard.com

Investment Company Institute. Monthly fund flow data. ici.org