Math Class is in Session

If you don't understand TVM, you're living on a prayer.

Time Value Of Money

Underlying the stock research techniques (fundamental, technical analysis, cocktail parties) and investment philosophies (value, growth, buying whatever went up yesterday), there is one truth that cannot be ignored, or explained away. And the sooner you understand it, the better investor you’ll be.

A dollar today is worth more than a dollar tomorrow.

This is partly due to inflation, but primarily because today’s dollar can be invested immediately and begin compounding now. Every investment analysis on every Bloomberg terminal, every spreadsheet and option pricing app, and every analyst’s buy or sell recommendation is based on the time-value of money.

How much is an investment worth today? It is worth the sum of future cash flows at a specific rate for a specific term. That’s it. But terminals, spreadsheets, apps, etc. can receive new inputs constantly and return the outputs in fractions of fractions of seconds.

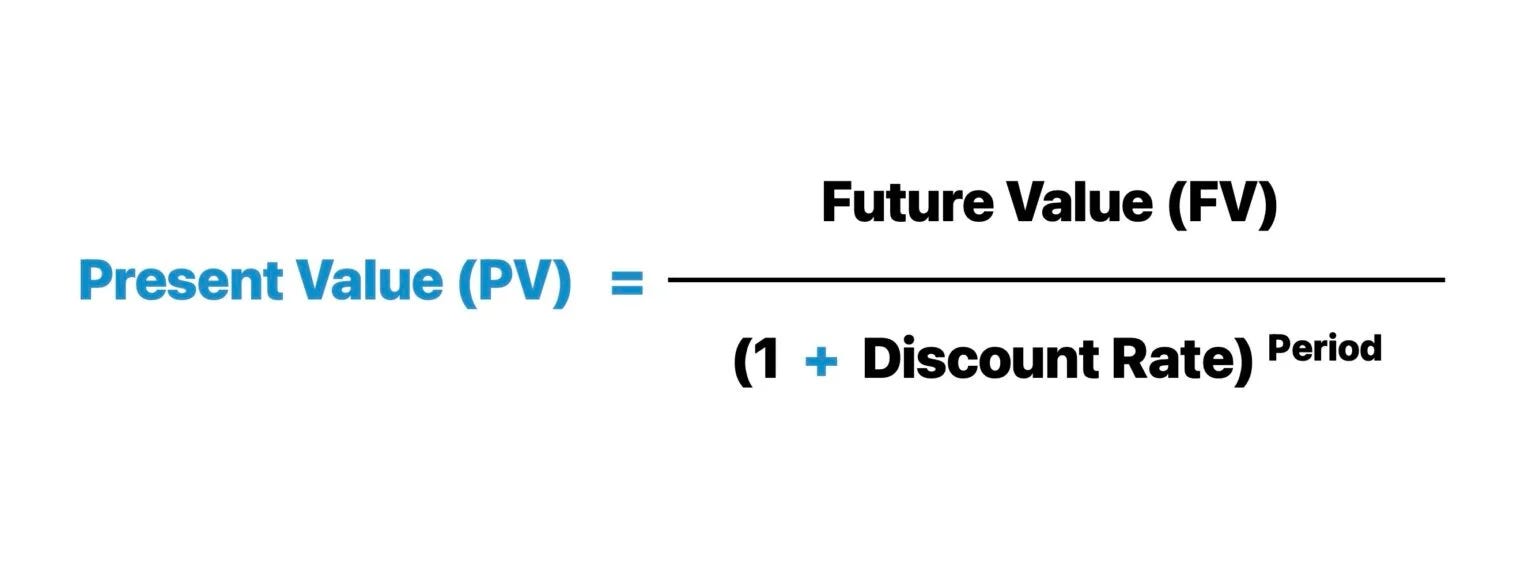

There’s even a formula for it:

Where:

PV = Present Value

FV = Future Value

r = rate of return (or discount rate)

n = number of periods

You probably see examples of it every day. Let’s say the Lottery is a $60 million jackpot. If you win, you can choose to get $2 million every year for 30 years, OR you can choose to get a lump sum of $10,448,879 immediately. In this example, if you choose to be paid over 30 years the Lottery organization can invest the $10.4 million (yes, I rounded) at 6% and earn enough to send you $2 million/year for 30 years – which equals $60 million.

PV = $60,000,000 ÷ (1 + 0.06)^30

PV = $60,000,000 ÷ 5.7435

PV = $10,448,879

But you say Hold On! 6% x 30 is only 180%. So, $10.4 million times 1.8 (180%) is only $18.7 million, and when added to the initial amount is only $29.1 million. Where did you get $60 million? That’s the secret sauce. The time-value of money involves compounding.

Each year’s 6% growth is not on the original value, but on ending value of the previous period. In this case, years. And if you think you can earn more than 6% return a year for 30 years (don’t forget taxes), then DEFINATELY take the lump sum.

The Math Is The Math

In the real world (assuming you are not a Lottery winner), a perfect example of the Present Value formula is a bond. When you purchase a bond, you know exactly what your cash flows will be over an exact period. In the real world, bonds typically pay interest twice a year, but I’m keeping it simple for math purposes.

If you spend $1,000 and receive 6% interest every year for 10 years, that’s $60/year. When the bond matures at the end of 10 years, you will receive your final interest payment PLUS the face value of the bond (in this case $1,000). Your EXACT return for 10 years has been 6%.

1000 = 1000 / (1 + 0.06)^10

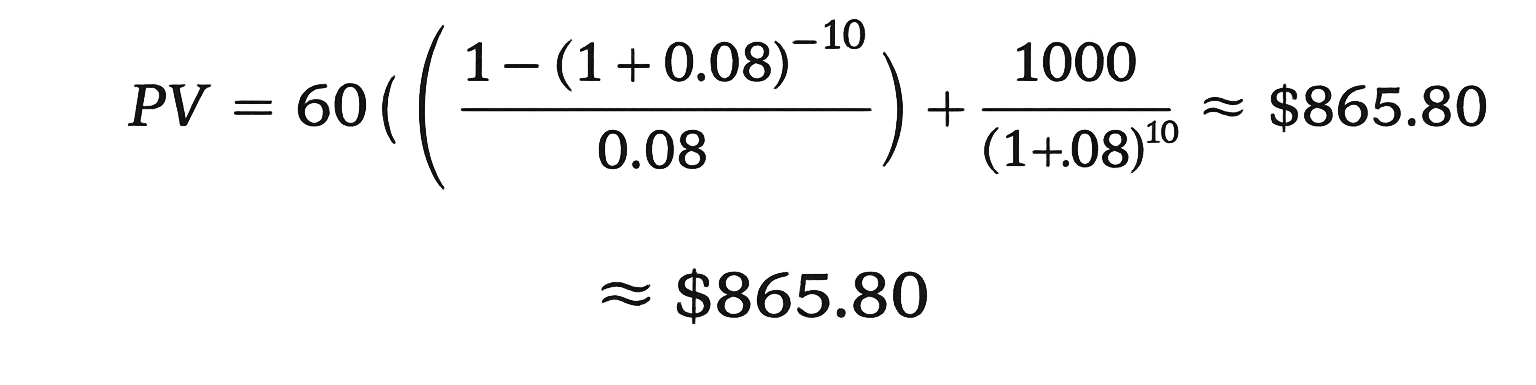

But let’s say you only want to buy the bond if you can get an 8% return. What is the highest price you’d pay for it? Calculate it, and show your work.

.

[Jeopardy music]

.

.

Pencils down.

First, the bad news. It’s hard.

For a cash flow of $60 per year for 10 years, and a cash flow of $1000 at the end of 10 years, to return an 8% compounded return you would want to pay no more than $865.80 for the $1,000 face value bond.

Now, the good news. We don’t have to do the calculations ourselves. Calculators, computers, newspapers, the internet, etc. do them for us. As investors, we simply have to decide if we accept the return as adequate for the risk we are taking. i.e., U.S. Treasury bonds have ZERO risk, We Bankrupt Businesses, Inc. bonds would have A LOT of risk. But you get to choose your risk levels.

Lesson 1: Financial math is hard, but necessary.

Lesson 2: In the real world you don’t need to do the calculations, you simply have to know how to use the results.

Lesson 2.5: Knowing that when interest rates go up, the present value (price) of bonds goes down - and inversely, when interest rates fall, the present value (price) of bonds goes down, is SO MUCH more important than being a calculator whiz yourself.

That’s It

Every valuation, every bid/ask, every new product, every financial plan (even Monte Carlo simulations), every insurance policy, etc. uses some variation of the present value formula.

Even Fundamental Stock Analysis

But how? We don’t know how long we’re going to hold a stock. Or what the future cash flows are; some companies don’t pay dividends and those that do can change the dividend amount over time. BTW, increasing dividends is very good, and cutting dividends is very bad. How fast will they grow earnings? What will they introduce next, and what will their competitors introduce next? What will my capital gains tax be when I sell it? Is their CEO close to retirement? And so on, and so forth ad infinitum.

That, as they say, is what makes a horse race. The truth is no one knows. Even Warren Buffett, by his own admission, makes investment decisions based on assumptions. Granted, he has better data and more experience, on which to base those assumptions.

If this sounds familiar, it should. It all goes back to:

Do you have a process?

Is it logical, defensible, and repeatable?

Do you apply it with discipline?

If you do, congratulations! You have the tools to examine your decisions (good and bad) and understand which assumptions were wrong, or right, and improve your investment process.

Why Is This Important?

Because everyone can do the math. But successful investors are the ones who can execute, examine, and then adjust and improve their assumptions. And who know how a little change in assumptions can have a huge change in decisions.

I hope I am playing some small part in the improvement, and enjoyment, of your investing. Carry on.

If you decide to use an investment professional as part of you process, you might enjoy The Insider’s Guide: How to Choose a Wealth Manager.